I never planned to open a dollar account.

For the longest time, my regular bank account did everything I needed it to do. Then, every now and again, something came up that didn't fit neatly into Nigeria's banking system: paying for an Electronic Travel Authorization (eTA) before a trip, subscribing to a service that only accepted dollar payments, or later, receiving money from abroad.

I could have opened a domiciliary account, like plenty of people still do. But I didn't want another trip to the bank, more paperwork, or another account that felt tied to branch hours and bureaucracy. So I started looking at the growing number of fintech apps promising USD accounts in minutes.

That first account became three: Grey, Chipper Cash, and Cleva.

But after months of using all of them, I've realised they're often mentioned in the same breath, but they solve very different problems.

/1. Grey

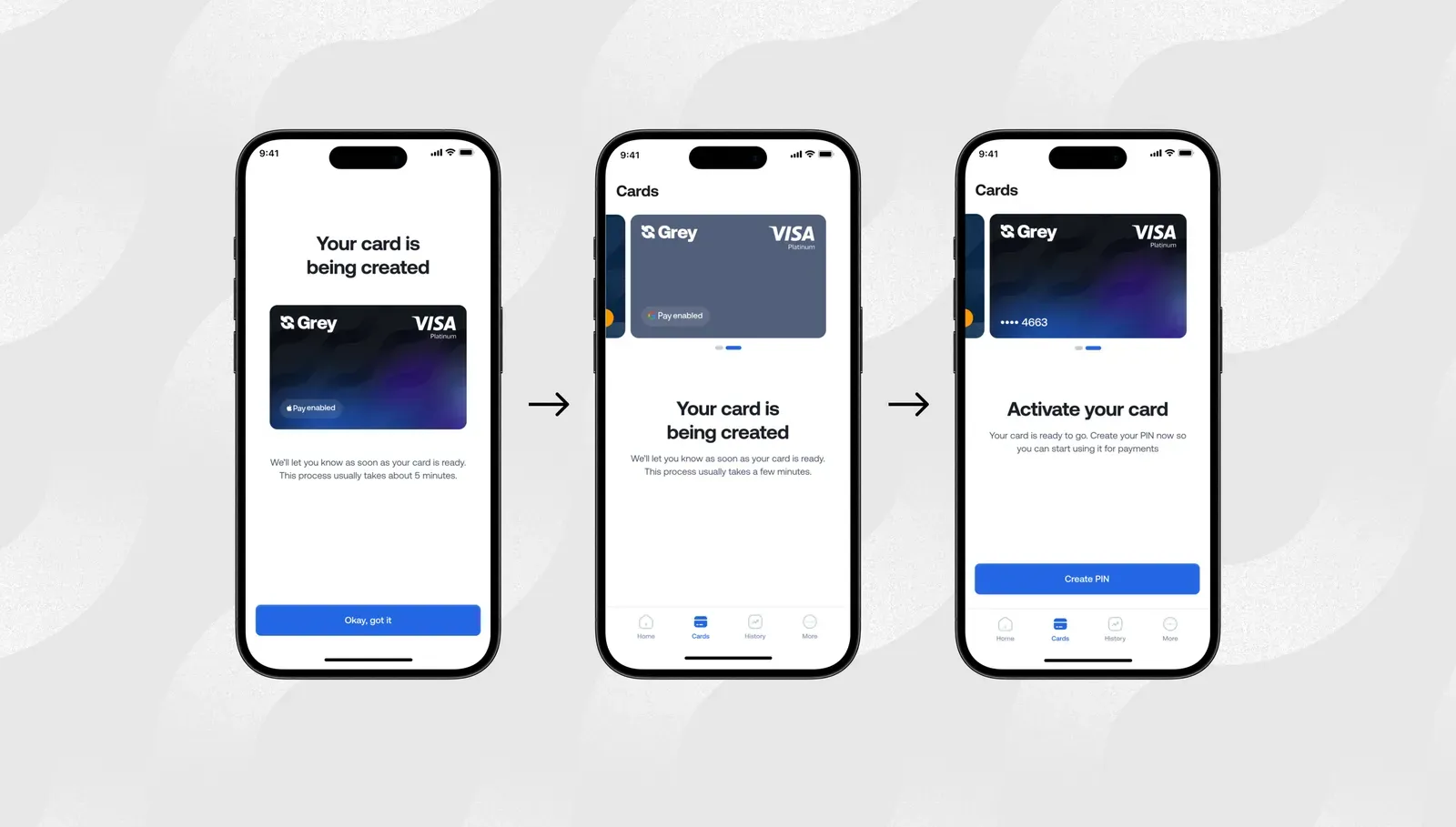

Grey was the first of the three I used, and it's still the account I associate most with getting paid from abroad. If someone asks me which platform feels closest to having an actual foreign bank account, this is usually the one I mention first.

To set it up, I downloaded the app, verified my identity with my national ID and a selfie, answered a few questions about what I do, and waited. The verification took about a day; in some cases, it can take longer, but once it was approved, I had USD, GBP, and EUR account details that I could share with clients or plug into platforms that support bank transfers.

Subscribe for free to continue reading this article

Subscribe SubscribeAlready Have an Account? Log In