Open, a neobank platform based in India has reportedly let go of around 50 employees and made a 50% cut to its founders' salaries in a bid to cut costs and improve the company's financial runway, according to a report by Entrackr.

Per the report, this move comes amidst a slow funding period, which has resulted in several fintech companies resorting to layoffs.

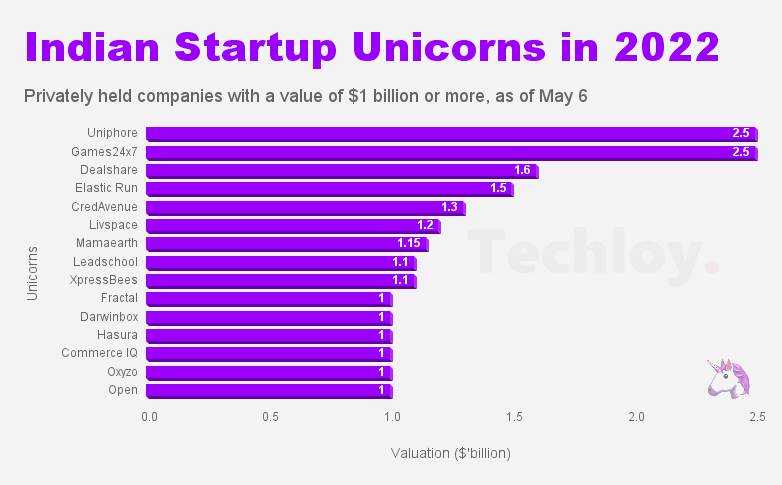

The neobank, which became the 100th unicorn from India, after raising $50 million – a figure lesser than it had planned – in its Series D round in 2022, has struggled to make money despite raising millions in the years prior.

In its fiscal year 2022, the company could only muster Rs 40.9 crore in revenue unable to reach the Rs 50 crore mark due to unfavourable market conditions. Furthermore, its losses also widened to Rs 167 crore from Rs 65.6 crore during the period.

Its market contenders such as Stashfin, Fi and Jupiter also failed to hit the mark, highlighting the financial challenges faced by the neobanking platform in India.

The report noted that the company confirmed the layoffs and pay cuts, but clarified that the layoffs affected only 47 employees, who were let go based on performance evaluations and the company has also outsourced some of its support functions to better manage growth and scale.

It also added that the company is still actively hiring for critical functions such as growth marketing, product, and sales.

The affected employees were reportedly only given one month's notice period worth of payment, with no severance package, sources say. Open has however not made any comment on this matter.