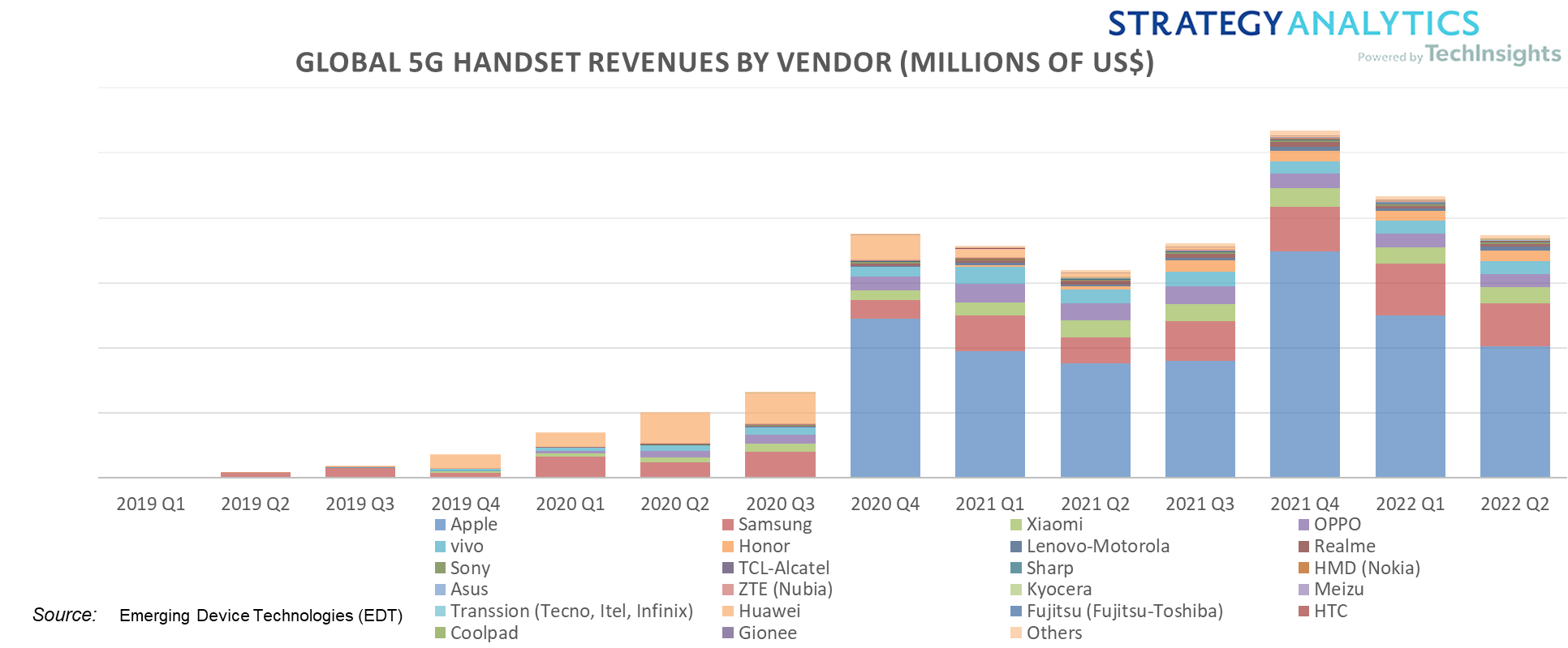

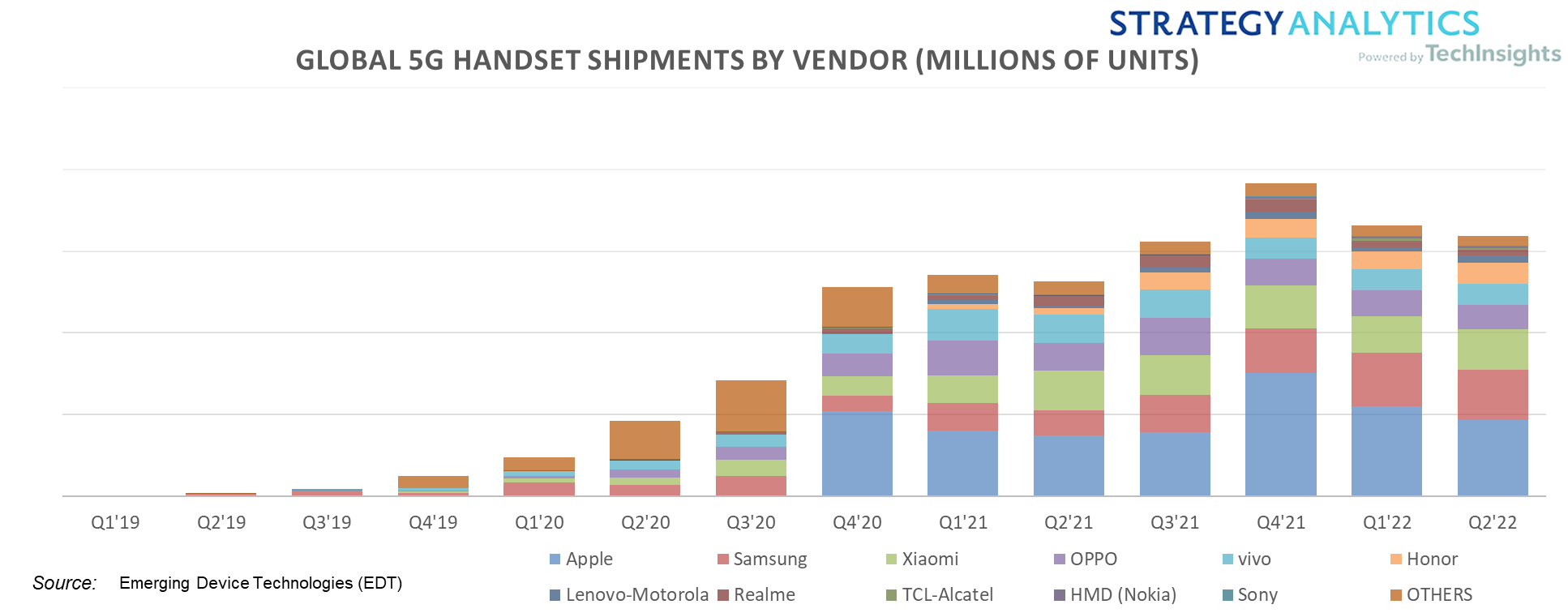

The sale of 5G enabled products has seen a massive growth since the adoption of the technology in late 2019, but in the wake of weakening demand, inflation, continued geopolitical tensions, and ongoing supply chain constraints, the smartphone industry is facing increasing headwinds from many fronts which have since impacted the growth of 5G revenue in 2022.

The COVID situation and lockdowns in China and geopolitical tensions in Ukraine and Russia have also strained the demand and production of 5G products and a consequent decline in revenue.

In particular, the pandemic has left deep scars in the form of lower investment, lower human capital, and tumbling global supply chains, all of which will possibly impact potential growth in the longer term.

But barring any new setbacks, it is expected that the abovementioned challenges would ease by the end of 2022, and the market to recover in 2023 with 5% growth.

According to estimates by Strategy Analytics, the market for 5G devices is expected to grow 25.5% year-on-year in 2022 and account for 53% of new shipments with nearly 700 million devices and an average selling price (ASP) of $608.

However, the recent global inflationary trends are hitting consumer demand and smartphone BoM costs, acting as a risk for the 2022 smartphone market.