According to Counterpoint, shipments of Extended Reality (XR) headsets including Augmented Reality (AR) and Virtual Reality (VR) crossed 1.1 million units in China in 2022.

Virtual Reality remains the dominant segment ahead of Augmented Reality within XR, contributing more than 95% to overall shipments in 2022. While the consumer segment did not see a major shift, volume growth was produced by enterprise deals, mostly in the education and training sectors.

Although the potential for further volume growth remains limited to the enterprise segment, the segment remains niche as the currently available headsets are not yet advanced enough to offer enticing use cases. Brands have now started to focus more on the consumer segment, particularly gaming to increase consumer traction.

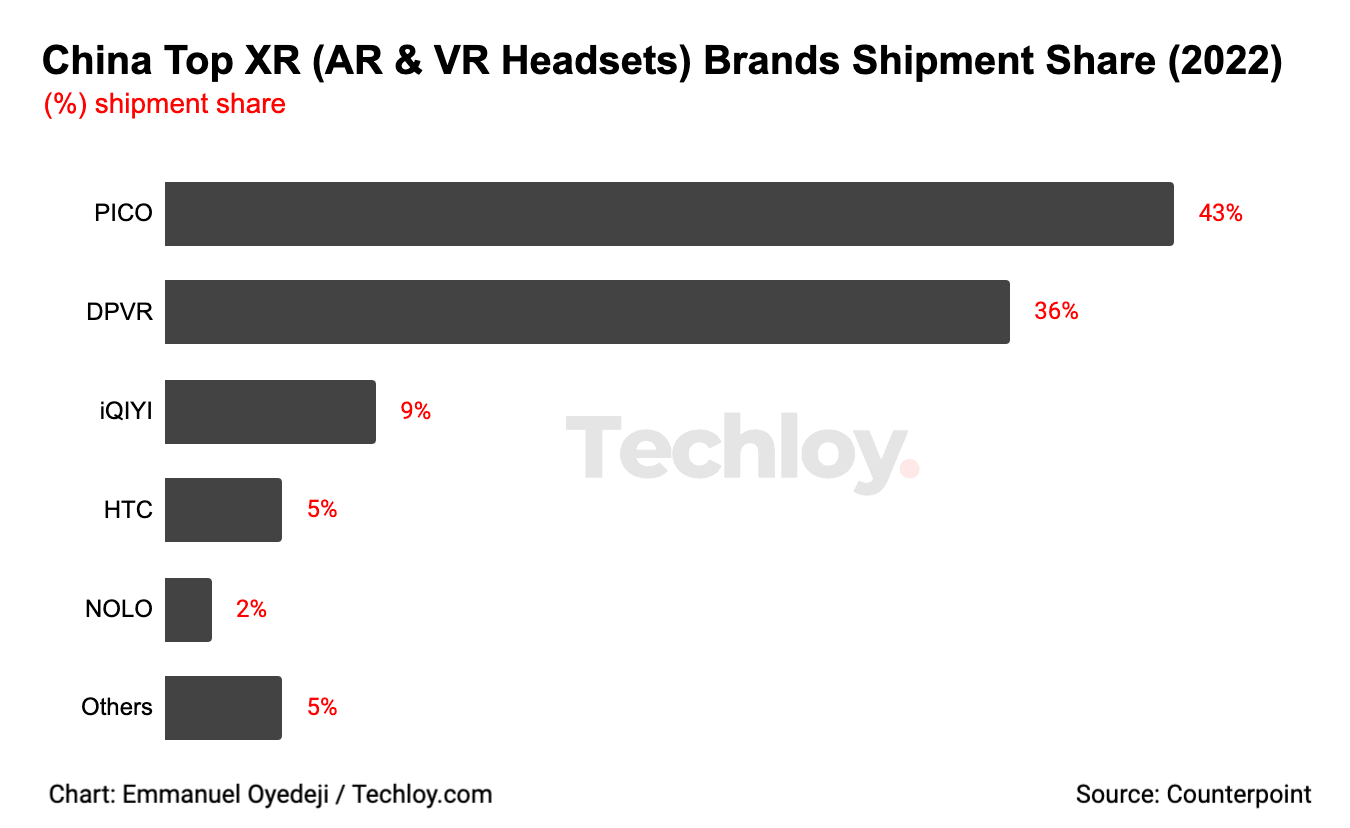

In the Chinese XR market, Pico is the number one brand in China’s XR market with a shipment share of 43% in 2022, followed by DPVR at 36%. iQIYI, HTC and NOLO, each of which captured a single-digit share, also made it to the top five.

It is noteworthy to mention that Pico was acquired by TikTok’s parent, ByteDance, and the additional financial, human and soft resources that ByteDance is pouring into the brand helped it to become a major player.